Mint, the popular personal finance site that won 2007’s TechCrunch40 conference, has closed a new $14 million Series C funding round. Silicon Alley Insider discovered the round in an SEC filing this morning, and we’ve just gotten off the phone with CEO Aaron Patzer, who confirmed the deal and filled us in on the details.

Mint, the popular personal finance site that won 2007’s TechCrunch40 conference, has closed a new $14 million Series C funding round. Silicon Alley Insider discovered the round in an SEC filing this morning, and we’ve just gotten off the phone with CEO Aaron Patzer, who confirmed the deal and filled us in on the details.

The $14 million round was led by DAG Ventures, and also includes newcomer Founder’s Fund. Existing investors Benchmark Capital, Shasta Ventures, First Round Capital, and Sherpalo Ventures all participated as well. Patzer declined to comment on the company’s valuation, but says that it is “decidedly an up round” and that it was preemptive. Mint hasn’t disclosed its revenues, but Patzer says that they’re up 8x year over year.

Since launching at TechCrunch40 in 2007, Mint has grown to 1.4 million registered users, tracking $175 billion in transactions and $47 billion in assets. The site also reports that it has identified $300 million in potential savings offers for its users. It primarily makes its money by generating leads for financial institutions, but it’s also sitting on a goldmine of user data that it hasn’t even begun to tap into yet.

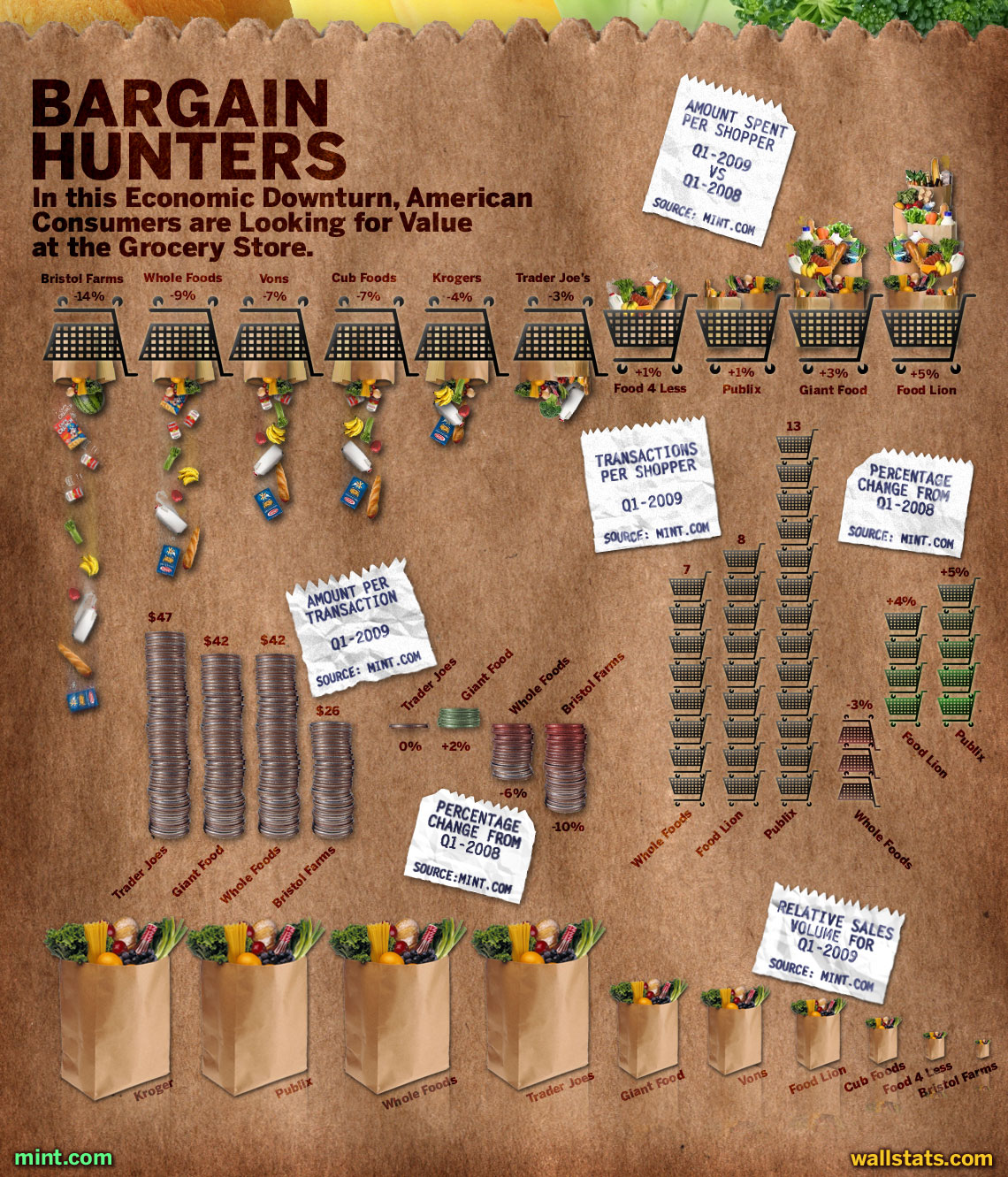

Because Mint pulls data directly from financial institutions, it knows where people are shopping and how much they’re spending. It can use this anonymized data in aggregate to track performance of entire industries or even individual stores. Up until now Mint hasn’t done anything with its merchant level data, but it’s beginning to open that up to press (see the chart below for a look at how the downturn is affecting grocery stores, which shows high end stores like Whole Foods and Bristol Farms taking a big hit in the down economy). This kind of data can be very valuable — don’t be surprised if we start seeing Mint leverage in other, more lucrative ways.