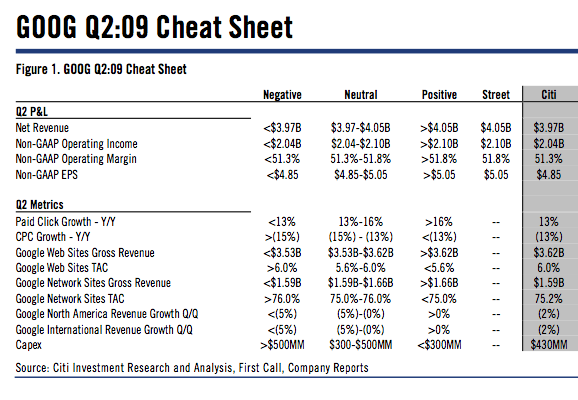

Google is scheduled to announce second quarter earnings on Thursday afternoon, and Citi analyst Mark Mahaney just sent out the handy cheat sheet above showing consensus estimates, as well as his own. The Street is looking for $4.05 billion in net revenues, Mahaney is predicting $3.97 billion. Anything above $4.05 billion would be viewed as positive, and anything below Mahaney’s estimate would be viewed as negative. Similarly, the Street consensus on non-GAAP EPS (earnings per share) is $5.05, while Mahaney thinks it will be 20 cents lower ($4.85). Anything between the two extremes would be viewed as neutral, according to his cheat sheet.

Mahaney is somewhat bearish compared to the consensus view, perhaps because of the continued economic difficulties and the deep funk the advertising industry is in. He expects revenues to increase only 2 percent on an annual basis, and to decline 3 percent on a quarterly basis. (Last quarter was the first time Google ever reported a sequential drop in revenues). His EPS estimate is only 5 percent higher than Google’s second quarter earnings a year ago, and 6 percent less than last quarter’s.

The cheat sheet also goes into how to evaluate Google’s key financial metrics, such as paid click revenue growth and average cost per click. Anything less than 13 percent paid click growth should be viewed as negative, anything above 16 percent as positive, and anything in between as neutral. He is modeling 13 percent growth. However, he expects the average cost per click to decline by more than 13 percent to $0.42.

Google can make its numbers if need be by tamping down discretionary capital expenditures, so keep an eye on that number as well. Anything above $500 million in CapEx wlil be seen as wasteful, anything below $300 million as frugal.

Will Google blow these estimates out of the water, or will it just keep treading?