It looks like PayPal is rolling out a more flexible payments API called Adaptive Payments. We’ve obtained a confidential document, which is embedded below, explaining the details of the new system. Basically the API is designed to give developers full access to PayPal’s features, allowing them a lot more freedom in building applications which include the ability to accept and distribute payments.

Very similar to Amazon’s Flexible Payments Service (FPS), the Adaptive Payments API handles payments between a sender of a payment and one or more receivers of the payment. Adaptive Payments allows almost the same functionality as FPS. The new API lets developers become a payment aggregator, which we are told is something against PayPal’s current Terms of Service. Amazon’s FPS also lets developers aggregate payments. Moreover, Paypal’s Adaptive Payments has built in micropayments support, another feature of FPS.

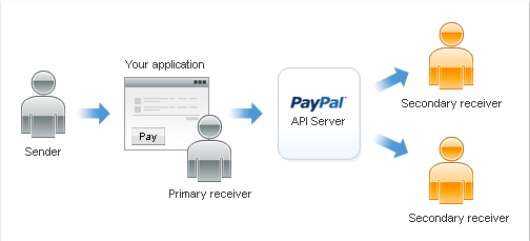

Some of the offerings of Adaptive Payments are sure to be attractive to developers. In what PayPal calls “Chained Payments,” developers can create applications that enable a sender to send a single payment to a primary receiver who may keep part of the payment and pay other, secondary receivers with the remainder of the funds. For example, an application might be an online travel agency that handles bookings for airfare, hotel reservations, and car rentals. The sender sees only the travel site as the primary receiver. But that site could allocate the payment for its commission and the actual cost of services provided by other merchants. PayPal would deduct the money from the sender’s account and deposit it in both the primary travel site’s account and the secondary receivers’ accounts.

Adaptive Payments will also offer “Parallel Payments,” which would let a sender send a single payment to multiple receivers. An example of this type of application might be a shopping cart that lets a buyer pay for items from several merchants with one payment. The shopping cart would allocate the payment to the merchants who actually provided the items. PayPal would then deduct money from the sender’s account and deposits it in the receivers’ accounts.

It’s unclear what PayPal’s pricing plan will be for Adaptive Payments and if it will be competitive with Amazon’s FPS pricing. Amazon has slowly been rolling out its competition to PayPal over the past few years, launching Amazon Payments and unveiling the beta of FPS. It isn’t easy for Amazon to replace PayPal, but it is going after developers to become the preferred payment mechanism on the Web. Perhaps PayPal is starting to feel the heat from FPS, which allows much more flexibility than PayPal’s Direct Payments API. Now, with its Adaptive Payments API in the works, PayPal is about to strike back.