Mint, the popular personal finance site that won 2007’s TechCrunch40, is launching a new feature called “Financial Fitness” which, strange as it may sound, adds an element of gaming to the service. Yes, it may sound like a bizarre combination at first – personal finance and fun aren’t exactly two things that go hand in hand. But it’s also a smart move on Mint’s part, as it looks to turn the mundane and often confusing activity of getting your financial affairs in order into something a bit more tolerable while increasing Mint’s engagement in the process. Mint is running the new feature in a private beta for a few weeks, and the first 500 TechCrunch readers to Email techcrunch-getfit@mint.com with the Email address they use on Mint.com will gain access.

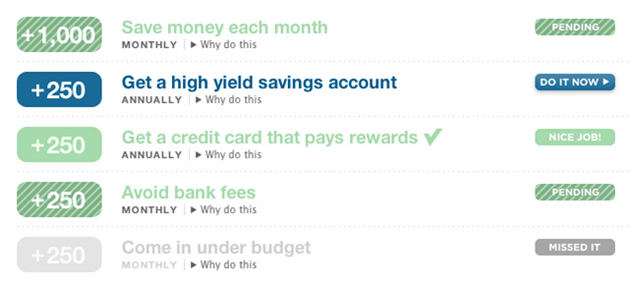

The game itself is fairly simple. It outlines five main principles that users should focus on on the road to financial fitness, including ‘spend less than you earn’, ‘manage credit and debt wisely’, and so on. Each of these core principles has a number of tasks associated with it, like ‘Avoid Bank Fees’ and ‘Come in under budget’. As you complete tasks, you are rewarded with points. Over time, you can earn merit badges for completing more difficult tasks, like being named as a “Financial Guru” for maintaining a 100% health status for an extended period of time. And then there’s the more tangible bonus of likely having more money than you started with.

Mint has studied the reward systems of games including Wii Fit, Warcraft, and Nike Fit as they built the game, looking to turn their virtual financial advisor into something a little more interesting than a wall of text. Of course, solving each of these tasks often involves the user interacting with a Mint feature or a referral to a partner site, which means Mint can effectively monetize the game as well.

I’m sure many people will initially react to the game with skepticism, as it isn’t exactly the first thing you’d expect at a finance site. But seemingly pointless gaming elements can be useful nonetheless: one need only take a look at foursquare, a fairly new application that is quite addictive because of its game-like nature. That said, these kind of point systems tend to work best when there is some kind of social element involved – be it through a rivalry with friends or an aggregated leader board. As a financial site Mint doesn’t seem well suited for this kind of competition (it would be a bit strange to make fun of my friends for having a poorer financial health than me), but I think the gaming aspect should work nonetheless.