Mint, the personal financial site that won TechCrunch40, continues to thrive even as our economy sinks deeper into an economic decline. The company has just been selected as a TechPioneer by the World Economic Forum in Davos, Switzerland – an honor only given to 34 companies worldwide (other winners in the tech space this year include Brightcove, Etsy, Mojix, and Slide, with past winners including Google, 23andMe, Infosys, and Mozilla). The World Economic Forum is an international organization aiming to help improve the world, and each TechPioneer is chosen for its contributions towards meeting that goal.

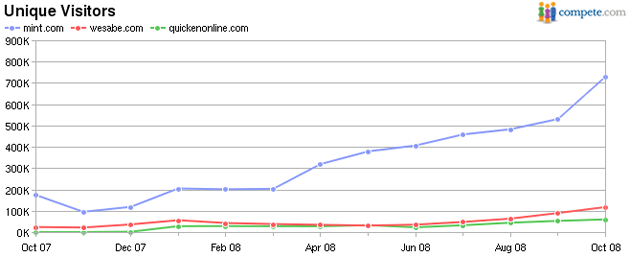

Since launching at TechCrunch40, Mint has amassed 620,000 users – 4 times more than its closest rival according to Compete. CEO Aaron Patzer says that the site is now tracking over $150 billion in total consumer spending, and has also revealed a number of telling trends that display how the economy seems to have impacted consumer spending.

According to Mint’s aggregated anonymized data, overall spending has dropped $400 in the last year, with half of that coming in the last two months. Starbucks spending has dropped around 10% (Starbucks has recently reported a 7% drop in month over month revenue). This kind of data could be incredibly valuable to businesses as a means of predicting spending trends – don’t be surprised if Mint begins offering a premium service for businesses who would gladly pay for aggregated spending totals.

Mint is also going increasingly mobile. Earlier this month the site added SMS support for account updates (text BAL to 696468 (MYMINT) for updates), and a native iPhone application is on the way.