![]()

Last month, peer-to-peer lender Prosper stopped all new lending on its site because of scrutiny by the SEC. Prosper agreed to register under the Securities Act, a process which can take months.

Yesterday, the SEC issued its formal cease-and-desist letter (embedded below or download PDF), outlining its reasoning for characterizing Prosper as a seller of investment, something prosper had vigorously resisted in the past by arguing that it was merely a marketplace matching lenders and borrowers. But the SEC is having none of that.

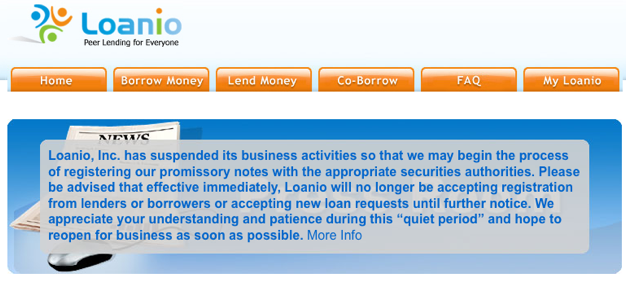

And it is not just Prosper, but all P2P lenders, that are on notice. Loanio, a new entrant into the P2P lending arena that just launched last month, has suspended new loans until it registers with the SEC as well (see notice below). And last April, competitor Lending Club was the first P2P lender to temporarily cease operations (the SEC approved its registration, and its members are now lending again in about half the states, including California which gave it the go-ahead last week).

The SEC letter makes clear why it considers Prosper a seller of securities and why it should be regulated by the SEC:

Thus, the Prosper notes are securities under Reves because: (i) Prosper lenders are motivated by an expected return on their funds; (ii) the Prosper loans are offered to the general public; (iii) a reasonable investor would likely expect that the Prosper loans are investments; and (iv) there is no alternate regulatory scheme that reduces the risks to investors presented by the platform.

Even though Prosper is not lending the money itself, the loans would not exist without Prosper. The letter gets into some more detail:

The notes offered by Prosper are investments. Lenders expect a profit on their investments in the form of interest, which is at a rate generally higher than that available from depository accounts at financial institutions. Prosper’s website has included statements that the Prosper notes provide returns superior to those offered by alternative investments such as equity stocks, CDs and money markets.

Lenders rely on the efforts of Prosper because Prosper’s efforts are instrumental to realizing a return on the lenders’ investments. . . . Prosper established and maintains the website platform, without which none of the loan transactions could be effected. Prosper provides mechanisms for attracting lenders and borrowers, facilitating the exchange of information between borrowers and lenders, coordinating bids, and effecting the loans. It provides borrower information to potential lenders via the loan listings, including credit ratings.

. . . Furthermore, under the terms of the notes, Prosper has the sole right to act as loan servicer of the notes. In this capacity, Prosper collects repayments of loans and interest, contacts delinquent borrowers for repayment, and reports loan payments and delinquencies to credit reporting agencies. Prosper also exclusively manages the process of referring delinquent loans to collection agencies for payment, and selling defaulted loans to debt purchasers. Since the lender does not know the borrower’s identity, the lender would be unable in any event to pursue his or her rights as a noteholder in the event of default.

. . . Rather, the Prosper lenders rely on Prosper’s continued operation of the platform in order to transact and to recoup any gain on their investments.

Obviously, any startup hoping to get into P2P lending should read this letter. But this reasoning probably also applies to other investment sites, such as social stock-picking sites, hoping to turn the information on their sites into investment products.

http://viewer.docstoc.com/

SEC Cease And Desist Order To Prosper – Get more Legal Forms