BillMonk is a new service that allows people to easily keep track of financial debts among friends. It’s a simple idea and they’ve executed well.

The idea is a user who wants to report a debt owed to him or her (such as a shared bill), or an IOU to another person, simply enters it on BillMonk. This is very easy to do on BillMonk, even for more complicated transactions like a bill shared among a lot of people. You simply input the amount of the bill and the email addresses for those who participated. There is also an SMS feature to allow users to text in bills on the phone.

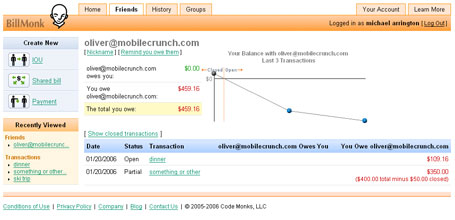

I like the way BillMonk keeps track of all of the various transactions a user has with different people, and the current amount owed at any given time. For instance, if I buy dinner for my friend Orli Yakuel and we decide to split the $100 bill, and later I owe her $8 for coffee, BillMonk knows that she only owes me a total of $42. When I tell BillMonk that she’s paid me $20, it automatically lowers the amount owed to me to $22.

Of course, if the people I am emailing are not yet using the service, they can sign up. So they’ve got the viral angle covered.

It’s useful, and really easy to use without FAQ references. There is also a way to SMS bills in via a mobile device. As of now, however, they have not integrated paypal or any other payment API.

Scott Loftesness and John Cook have also recently written about BillMonk. The company was founded by Gaurav Oberoi and Chuck Groom, who previously worked at Amazon.